State Space Models with a Common Stochastic Variance

Introduction

In the paper `State Space Models with a Common Stochastic Variance' by

, an estimation method is presented for combinations

of the stochastic volatility model

and the general linear state space model

with a common fixed variance

s2, that is

where y

t is a p ×1 vector of observations, c

t is a p×1 vector of fixed effects (possibly containing regressor

variables),

at is a m

a ×1

vector of unobserved states and

et is a r×1 vector of disturbances. The system matrices Z

t, T

t,

G

t and H

t are assumed to be fixed for all time points

t=1,

¼,n. Unknown elements of the system matrices will be treated

as parameters to be estimated by the method of maximum likelihood.

The two models are easily combined by changing the common fixed variance

s2 in (

2) with the time varying variance of

(

1).

This page presents the programs used in obtaining the results.

Programs and installation

The package

ssfsv4.zip contains the necessary files and data for

estimating models in state space using simulated maximum likelihood.

Unpack the file to a directory of your choice. For graphical output,

either the original

OxDraw routines of

Ox 7 can be

used, or alternatively one can install

GnuDraw.

The programs depend on the extended version of

SsfPack, of

Siem Jan Koopman.

The installation file contains a

readme.txt

explaining the contents of the package. Most instructive is the program

ssfsvest5.ox which estimates an SV model based on

settings in

simox.dec.

Some usage hints

The package declares an object of type

SSFSV(), deriving from the

Ox

Modelbase

class. Using the standard Modelbase routines, a dataset should be set

up, selecting the exogenous variables as usual.

The model is specified using a call similar to

Ssfsv.ChooseModel(<CMP_LEVEL, .05, 0, 0;

CMP_SEAS_DUMMY, .025, 12, 0;

CMP_IRREG, .15, 0, 0;

CMP_SV, .2, 0, .95>);

which would specify a local level model with seasonal effects, and a

common stochastic variance component with, initially, standard deviation

sx = 0.2 and persistence

f = 0.95.

After setting up the model, estimation is done with the usual call to

Ssfsv.Estimate();

Note that estimation can be time consuming, especially if the number of

importance samples is large.

Selected results

With the above settings in the file

declinfl/infl_llssv.dec copied over

simox.dec, running the program

oxl ssfsvest5

results in Ox output as displayed in

Table

1 below, equal to results in .

Graphical output is created to show the

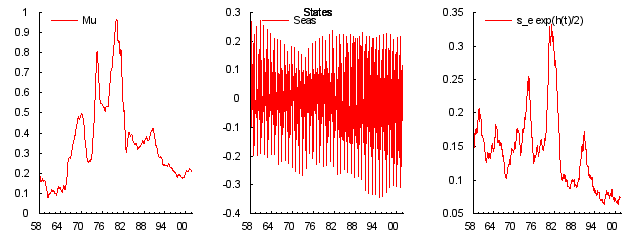

states estimates as in Figure

1, weights, residual

analysis and much more.

Table 1: Results of optimisation

---- SsfSV ----

The estimation sample is: 1957 (1) - 2001 (9)

The dependent variable is: dLcuur

Coefficient Confidence bounds Score

s(Lev) 0.0296983 [ 0.02042, 0.04319] <2.423e-07>

s(Seas_dum) 0.0370710 [ 0.02506, 0.05484] <3.642e-07>

s(Irr) 0.139992 [ 0.1061, 0.1847] <1.805e-06>

s(SV) 0.216399 [ 0.1467, 0.3192] <2.384e-06>

phi(SV) 0.963198 [ 0.9193, 0.9837] <-2.103e-06>

log-likelihood 153.137492

no. of observations 537 no. of parameters 5

AIC.T -296.274984 AIC -0.551722502

mean(dLcuur) 0.350417 var(dLcuur) 0.0889883

Using maximum likelihood estimation and transformed parameters

with the exact likelihood

in a time of 25:05.61

Table 2: State estimates as for the model with common stochastic

variance

Routines in the package

Apart from the normal Modelbase routines, some added functions

provided are

-

#import "include/ssfsv"

ChooseModel(const mStsm);

- mStsm

- in: Matrix to indicate the type of State Space model. Apart from the

standard Ssfpack elements, also components for an SV model, for GARCH or

for ARMA are possible. See the declaration files for examples.

[

Top]

-

#import "include/ssfsv"

ChooseSVRep(const iMaxRep, const iSimSV);

ChooseSVRep(const iMaxRep, const iSimSV, const bApprox);

- iMaxRep

- in: integer, indicating the maximum number of repetitions to use

while searching for the approximating model (default=50, use -1 to keep

old value).

- iSimSV

- in: integer, number of simulations used in the importance sampler

(default=250, use -1 to keep old value).

- bApprox

- in: boolean, indicating if an approximative (but quicker) likelihood

should be used (default=FALSE).

[

Top]

-

#import "include/ssfsv"

ChooseTransform(const bUseTransform);

- bUseTransform

- in: boolean, indicating if a transformation of the parameters should

be used or not (default=TRUE)

[

Top]

-

#import "include/ssfsv"

SetSampleZoom(const iZoom1, const iZoom2);

- iZoom1, iZoom2

- in: integers, indicating indices of first and last observation to

which we zoom in, e.g. when looking at the weight graphs.

[

Top]

-

#import "include/ssfsv"

SSFSVLikelihood(const vP, const adFunc, const avScore, const amHessian);

- vP, adFunc, avScore, amHessian

- See MaxBFGS; this routine provides the likelihood function of the

model

[

Top]

-

#import "include/ssfsv"

GenerateSsf(const vP, asName);

- vP

- in: Vector of parameters of the model

- asName

- in: String, or array of strings, with name of variable, under which

the newly generated data is stored in the database.

[

Top]

-

#import "include/ssfsv"

GetISWeights();

- Return value

- mWgt: 2 x iSim matrix with importance sampler weights.

[

Top]

-

#import "include/ssfsv"

GetConfBounds();

- Return value

- mLU: iP x 2 matrix with the bounds of the (non-symmetric, if

transformed parameters were used) confidence region.

[

Top]

-

#import "include/ssfsv"

SaveGraphics(const sGraphbase);

- sGraphbase

- in: String with the basename for saving graphics; if the empty

string is given, no graphs are saved.

[

Top]

-

#import "include/ssfsv"

TestAuxResiduals(vbSel, vbPlot, const dLimit, const bWrite);

TestCorrelogram();

TestFinal();

TestGoodFit();

TestGraphics(vbPlot, const bFilt, const iaLog, const iNLSeas);

TestISWeightGraphs(dQ);

TestNormality(const vRes, const sName);

TestResiduals(vbPlot, const iLag, const bWrite);

TestParameterGraphs();

TestSummary(const bShow);

TestWeightGraphs(const vP, iW);

- Set of testing routines, see actual programs for their usage.

[

Top]

Bibliography

Koopman, S. J. and Bos, C. S. 2004

, `State space models with a common stochastic variance', Journal of

Business and Economic Statistics 22(3), 346-357. [ http ]

File translated from

TEX

by

TTH,

version 3.77.

On 22 Mar 2011, 16:09.